As independent schools seek to attract and retain top leadership talent, many have expanded their benefit offerings to include a non-governmental 457(b) plan. These plans are often reserved for the Head of School, but some institutions extend eligibility to the broader executive team or “Top Hat” educators—such as the CFO, Director of Development, Assistant/Associate Heads, and other highly compensated employees (HCEs).

What Is a Non-Governmental 457(b) Plan?

A non-governmental 457(b) is a non-qualified deferred compensation plan that allows eligible employees to defer a portion of their salary into a tax-advantaged account—reducing taxable income beyond what’s contributed to a 403(b) or 401(k). Unlike governmental 457 plans, these accounts are subject to different rules and cannot be rolled into IRAs or qualified plans.

Key Features and Distinctions

- Contributions are made pre-tax and taxed upon withdrawal

- Assets remain the property of the employer until distributed

- Plans are limited to a select group of HCEs

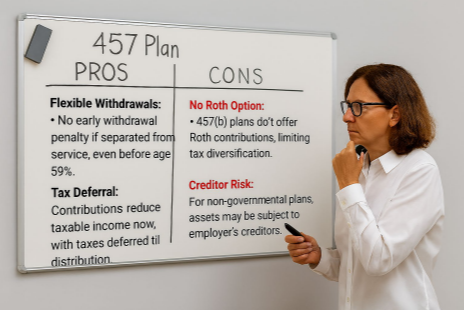

- Withdrawals before age 59½ are not subject to the 10% early withdrawal penalty

- 457(b) plans serve as a strategic incentive for senior administrators to stay with the school

- Assets are not held in trust and are exposed to the employer’s creditors

How These Plans Work

- Employee Contributions: Pre-tax only; taxed upon distribution

- Employer Contributions: Also pre-tax; same tax treatment

- Eligibility: Defined by the plan document, limited to HCEs

- Required Minimum Distributions (RMDs): Apply to non-governmental 457(b) accounts

Key Considerations Before Funding

Before contributing to your school’s 457(b) plan, weigh the following:

- Institutional Risk: Because assets remain the school’s property until distributed, assess the school’s financial health and your comfort with creditor exposure

- Career Trajectory: If you leave before retirement, your plan may require distribution upon departure—potentially triggering higher taxes

- Tax Implications: For older educators, contributing to a 457(b) plan can reduce overall tax liability over time, especially if distributions occur during lower-income retirement years. For younger educators, however, rising income from career changes may lead to higher tax rates—potentially resulting in greater taxes on 457(b) withdrawals than the savings realized during contribution years.

- Alternative Savings: For the younger school administrator who values job mobility, a taxable brokerage account may offer greater flexibility and control, especially if their tax bracket or liquidity needs shift

Common Questions

Is there a Roth option?

No. Roth contributions are not permitted in non-governmental 457(b) plans.

Are these plans portable?

Only under specific conditions. Confirm with your new school’s plan administrator.

Can I roll the 457(b) into an IRA or 403(b)/401(k)?

No. Rollovers are generally restricted to another non-governmental 457(b) plan.

Are assets protected from creditors?

No. Unlike IRAs and qualified retirement plans, non-governmental 457(b) assets are not held in trust and are subject to the employer’s creditors.

Case Studies: When It Makes Sense—and When It Doesn’t

�� Example 1: Strategic Use

Mr. Charles Chips, age 50, is newly appointed Head of School at Hogwarts, a well-endowed and financially stable boarding school. His salary is $500,000, and he plans to retire in six years—before age 59½. His spouse, Charlee Chips, is a high-earning attorney. Both are maxing out their 403(b), 401(k), and Backdoor Roth IRAs. Their combined income places them in the 37% tax bracket, and they expect to be in a lower bracket in retirement.

Why it makes sense:

- Charles wants to defer additional income beyond 403(b) and Roth limits

- The Chips value penalty-free access before age 59½

- They trust Hogwarts’ solvency and Charles is unlikely to change employers

- Their financial planner is helping them model lower taxable income in retirement

� Example 2: Proceed with Caution

Ms. Sally Smart, Assistant Head at Risk Academy, earns $200,000 and is single. She’s considering leadership roles at other schools within 2–3 years. Sally is funding her 403(b) and building a taxable brokerage account. She’s in the 24% marginal tax bracket but expects higher income in future roles. She’s concerned about creditor exposure and the lack of portability in Risk Academy’s 457(b) plan.

Why it doesn’t make sense:

- Sally may be forced to take distributions upon departure, triggering higher taxes

- She’s uncomfortable with the lack of asset protection and employer ownership

- She prefers flexibility and control over her retirement assets

- She’s wisely cautious about locking funds into a plan that may not transfer

Final Thoughts

Non-governmental 457(b) plans offer unique opportunities and risks. Their value depends on your career path, tax situation, and trust in your institution’s financial health. Modeling various scenarios with a financial planning partner can help clarify whether this strategy aligns with your long-term goals.

David Brown was the Chief Financial Officer/Business Administrator at Blanchard Memorial School, Groton School, Alexander Dawson School, Rippowam Cisqua School, and Portsmouth Abbey & School over a 23-year school career. During that time, he advised and/or helped heads and administrators assemble and negotiate benefit packages that would ensure a comfortable life through “end of plan”. For over 10-years Dave has helped his clients effectively plan, save, and invest to and spend appropriately through retirement.

For personalized financial planning and/or investment guidance, contact Clear Skies Planning & Wealth Strategies at www.clearskieswealthplanning.com or directly at 720-833-8611.

Clear Skies Planning & Wealth Strategies, Inc provides advisory services through XY Investment Solutions, LLC, an SEC registered investment advisor. All views included in this communication are subject to change. Please contact Clear Skies Planning & Wealth Strategies to receive a copy of our Form ADV and other disclosure information.